|

In 2011, with the eurozone still recovering from 2008 2009s global recession, the ECB hiked rates twiceonly for the economy to fall back into recession again as the eurozones sovereign debt crisis erupted. Many deemed the hikes a monetary mistake. With eurozone GDP growth easing to its slowest rate of this expansion in Q3, some worry the ECBs move to reduce monthly asset purchases to 15 billion in Octoberand plans to end the program after Decemberare similarly ill-timed. If the ECB stops its monetary support, doesnt that increase eurozone economic risks? In our view, no. Contrary to popular belief, we think the ECBs eventual exit from quantitative easing (QE) should help, not hurt, the eurozones loan growth and economya positive surprise for eurozone stocks.

QEs end elsewhere wasnt a negative. Despite much fretting, prior UK and US QE exits occurred without incident. The BOE stopped its asset purchases in late 2012, and the Feds bond buying binge finally ceased in October 2014. Both times, many thought the UKs and USs economiesand financial systemswouldnt withstand the withdrawal. Butlo and behold!their economies and markets didnt implode. In 2013, UK economic growth accelerated and stocks rose. US economic growth accelerated during 2014s tapering. In 2015, US growth slowed and stocks were flat, but this was mostly due to oils price collapse and its impact on investment and earningsnot QE withdrawalwhich subsequent growth has proved. We expect QEs end to go similarly fine in the eurozone.

Yet, in our view, a common misperception keeps many from cheering QEs demise. Among the greatest tricks central banks ever pulled is convincing the world QE is stimulus. QE supposedly works by lowering long-term interest rates, encouraging lending. But though the lower interest rates = more lending theory may seem plausible, it obscures how monetary policy affects banks. Easy money requires balancing banks willingness to lend with folks desire to borrow. Banks extend loans only when profit margins make the risk worthwhile, a factor largely determined by the yield curve (or spread)the difference between short-term and long-term interest rates. Because banks borrow short and lend long, the more long rates exceed short, the more profitable bank lending is, encouraging them to lend. By buying large amounts of eurozone long bonds, we think the ECBs QE program lowered long-term interest rates, but it also flattened the yield curve and discouraged banks from lending. In our view, that stifled growth rather than stimulating it.

The good news, however, is the ECB has scaled back its bond purchases substantially over the last two years, helping lift long rates, lending and growth. In December 2016, the ECB first signaled its plan to reduce average monthly bond purchases from 80 to 60 billion the following April. Another taperfrom 60 to 30 billiontook effect in January 2018, followed by last months.

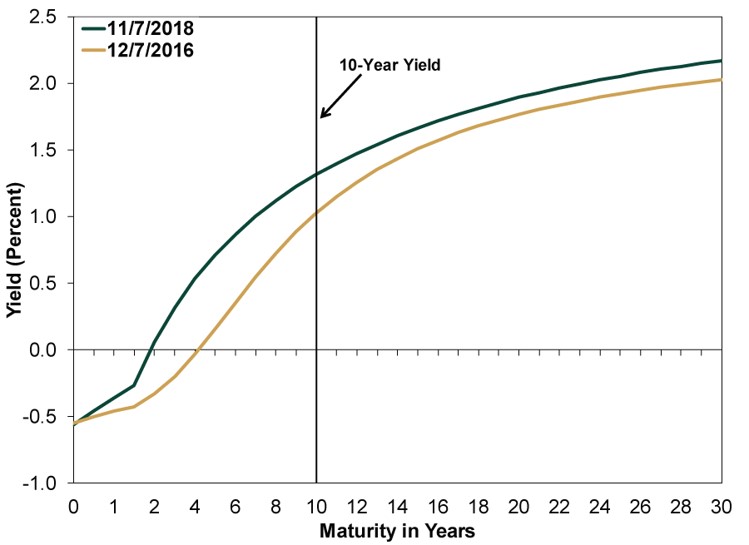

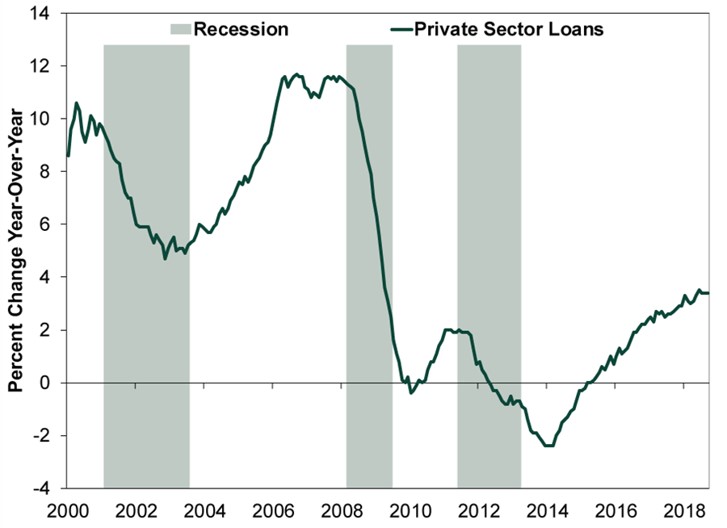

To see taperings impact, consider the ECBs eurozone yield curve. Now, there is of course no collective eurozone debtthe ECB averages euro countries yields to calculate this as a proxy. But we believe it is a helpful, concise illustration of taperings impact. From the day before the ECB first broached tapering to yesterday, the eurozone yield curve spread (10-year yield minus 3-month yield) steepened from 1.6 percentage point to 1.9 percentage points.(Exhibit 1) Loan growth accelerated from 2.2% y/y in November 2016 to 3.4% as of September, which continues the upward trend from 2014 after the eurozone began its economic recovery. (Exhibit 2)

Exhibit 1: Eurozone Yield Curve Steepened as ECB Tapered

Source: ECB, as of 11/8/2018. ECB all bonds yield curve on 12/7/2016 and 11/7/2018. The ECB announced its first asset purchase reduction on 12/8/2016.

Exhibit 2: Loan Growth Has Accelerated

Source: ECB, as of 11/5/2018. Private sector adjusted loans (i.e. adjusted for loan sales, securitization and notional cash pooling), January 2000 September 2018.

Despite the stimulus narrative, loan growths acceleration as the ECB has reduced bond purchases shows tapering hasnt hurt. The ECBs latest Q3 bank lending survey also points to easing credit standards and financial institutions increased willingness to lend. Rising business and household demand for and access to credit should continue driving broad economic growth.

In our view, the risk isnt that ECB ends QE and pulls the punchbowl. We think the real risk is if the ECB overreacts to recent data by extending or even adding to QE. Markets have seemingly already been pricing in the end. U-turning now would probably extend uncertainty by creating a new round of angst over when QE would end. Returning to normal should allow people to get over it. If QE ends and the eurozone economy doesnt tank, folks should realize the economy doesnt need the ECBs support. In our view, that would likely give investors more confidence, help improving sentiment and boost eurozone stocks. Negative sentiment surrounding QEs end and its positive impact in reality presents a bullish disconnectand opportunityfor investors.

|