|

TrackMacros artificial brain has been analyzing macro risks for equity holders monthly for now more than four years. TrackMacro takes two viewpoints for each country: one internal, the other external.

(i) The internal viewpoint focuses on inflation, growth, and the countrys competitiveness in terms of currency, equity and bond valuations, and the cost of energy.

(ii) The external viewpoint tracks international trade and liquidity in USD.

Trade and liquidity are the two faces of Janus, one looking at economics and the other at finance. In the case of conflicting conclusions, economics takes precedence.

Entering December, Trade turned positive from neutral, and TrackMacros world equity allocations jumped from 66% to more than 80%, despite longstanding liquidity issues.

Is TrackMacro misreading international trade? If not, how can trade be accelerating in an environment of rarefied liquidity?

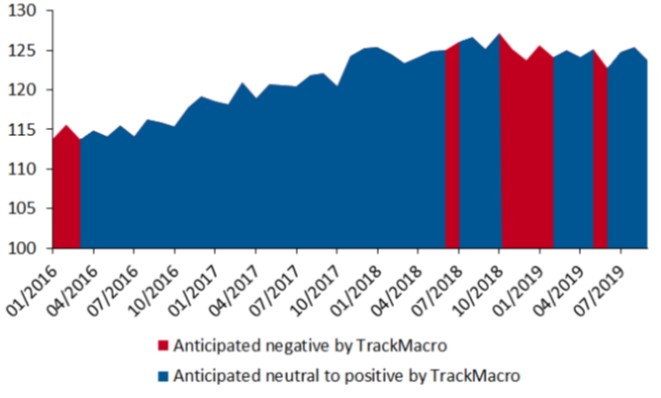

TrackMacros Leading Indicator on Trade

World trade volumes are published by the Netherlands Bureau for Economic Policy Analysis with a three-months lag. TrackMacro adjusts the trends by observing the assets historically correlated to international trade in the missing quarter.

Figure 1 on the next page shows the models ability to ring alarm bells appropriately, to warn for potential trade sluggishness and equity drawdown, which is TrackMacros primary role.

Fig 1. World trade in volume anticipated by TrackMacro 3 months in advance

Source: Bloomberg MWT VWT Index, TrackMacro

The models success is confirmed over twenty years of history. Its failures appear naturally during political shocks, such as October 2018, or May 2019, when political tensions on trade agreements between the USA and China suddenly spiked. Politics, however, may not be the sole reason for a sluggish world trade since the end of 2017.

The Worlds Shortage of USD

TrackMacro doesnt follow credit multipliers, but tracks the international monetary base in USD, i.e., the domestic base and the USD deposits of foreign central banks at the Federal Reserve. Foreign central banks reserves are, to a certain extent, counterparty to the US trade deficit and to the printing of new local money by central banks to buy such dollars from the private sector. The mechanism was described by Jacques Rueff under the name of: double pyramid of credit.

The world has been suffering from a shortage of USD for 25 months in a row, which is the longest period ever, since the end of the Gold Standard in 1971. This might explain the USDs surprizing strength during the last two years and the fact that world trade has completely flattened over the period.

Could the lack of USD be a structural issue?

The Dangerous Base Effect on USD Dominance

75% of the $100 bills in the world are circulating offshore. 90% of the worlds foreign exchange transactions and 50% of the international trade settlements are denominated in USD. Dollar dominance is far from over. Furthermore, the US Federal deficit, at 4.6% of the GDP, is at a high level for a time of economic expansion. Its anticipated to remain in the 4.5% to 5% range for the next ten years. Dollars are therefore flowing out of the USA. But is this process enough to fulfil the dollars role in the settlement of international trade?

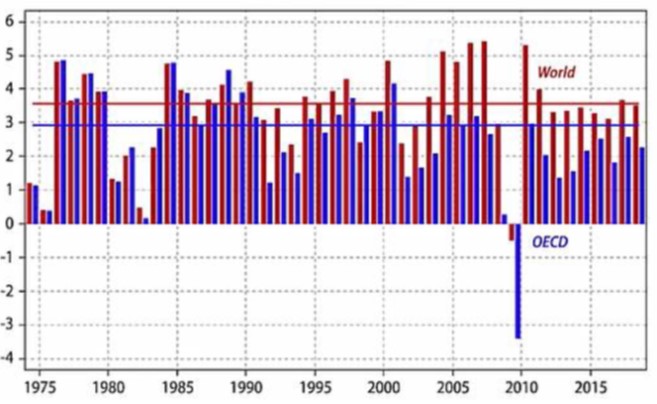

Emerging economies are growing faster than the USA, and faster than OECD countries in general. The supposed secular stagnation is therefore a myth for global businesses, as underlined by Anatole Kaletsky from Gavekal Research.

Figure 2 below shows that, unlike OECDs GDP, the worlds GDP growth isnt dwindling. What is dwindling is the USAs contribution to the worlds GDP, which now stands at 24%.

Fig 2. GDP Growth: Global and OECD - lines=Mean 1977-2007

Source: Anatole Kaletsky, Gavekal Data/Macrobond

If world trade grows in line with world GDP, at around 3.6% per annum, the need for dollars is +1.8% per annum to settle transactions, 50% of trade being denominated in USD. The US deficit, at 4.6% of the US GDP, only reaches 4.6%*24% = 1.1% of the worlds GDP.

The base effect of fast-growing emerging economies creates a structural shortage of USD.

Short-term and Long-term Solutions for USD Shortage

The long-term solution for a lack of USD is the emergence of new currencies, such as the CNY, for international trade settlements. This is a process which is already taking place, but at a pace that is too slow.

During the transition phase, the Federal Reserve still holds the key to global liquidity management. The renewal of Treasury purchases in October is a response to the shortage. The three main central banks in the world, the FED, the ECB, and the Bank of Japan, have now entered in a simultaneous round of Quantitative Easing.

Liquidity should improve in the foreseeable future and thus support the rebound of world trade, as is expected by TrackMacro.

|