|

It is the confluence of finance, dollars, liquidity and economics with or without recovery and the best scenario. The FOMC raising rates is supposed to confirm the brightest outlook, which would only lead to more extension in the credit cycle, and yet junk bonds traded as if the worst were only just around the corner. It isnt so much the selloff, though that is obviously important, but rather how increasingly the selloff is being treated as permanent.

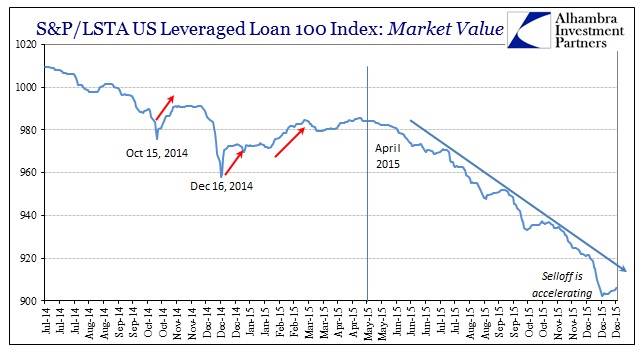

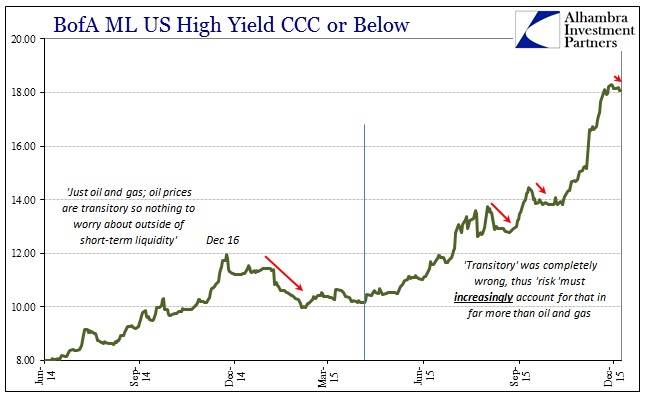

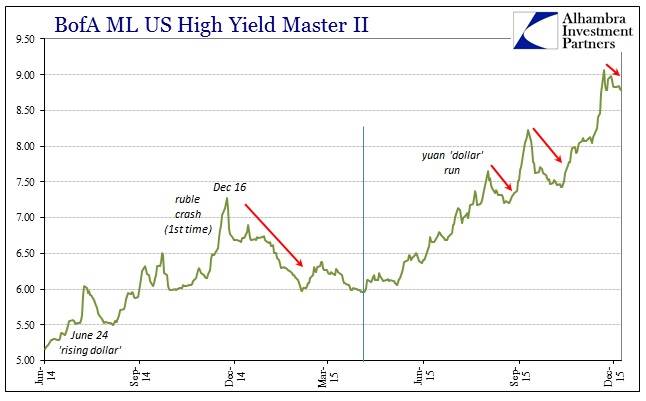

It is the expression of an obvious and apparently durable shift in risk perceptions, and I think it the most significant development. You can see it clearly in the changes this year to last. After the selloffs in October and December 2014, junk was bid in clear bargain hunting patterns of behavior. The rebound after last December lasted months and was quite significant even if it didnt quite bring prices and yields quite back to the full comfort of prior complacency.

This year, each discrete selloff was met instead by listlessness and palpable uninterest, including the past week or so after what was undoubtedly the most intense selloff yet. That leaves the waves of selling only pushing the idea of the continuation in the credit cycle further and further remote; bringing instead the sense of doom closer and closer. This alteration in outlook and perception really could not be more unmistakable:

It is not your typical market behavior; not at all the wall of worry that represents healthy skepticism and functional fundamental discounting but rather a get the hell out of Dodge and stay out. Not transitory at all, then, rather a paradigm shift that isnt yet even close to a new steady state. Welcome to 2016.

|