|

For a start, it is even misleading to talk of a great rotation. Rather, at any point in time, the market place consists of a certain stock of cash, bonds and equities, whose relative returns adjust depending on the relative supply/demand forces. An individual can rotate but the market in aggregate cannot, as the outstanding stock of assets must be held by someone. As such, the fact that investors currently own lots of bonds (vs. equities) is largely a reflection of strong supply.

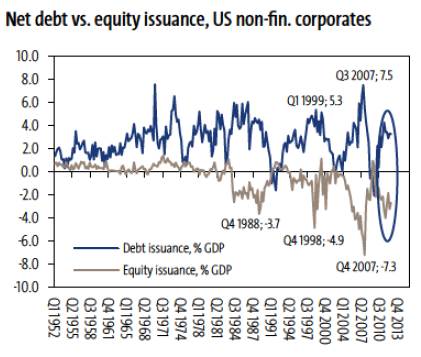

Indeed, the massive increase in leverage over the last decade has led the market capitalization of the bond market to rise. Meanwhile, the equity market has been shrinking with US companies using proceeds from debt issuance to buy back their own shares, taking advantage of the gap between (low) financing rates and (higher) cost of capital (see upper chart).

Is it possible, going forward, that higher demand for equities that are in short relative supply drives their prices up, and conversely for bonds? Clearly, such portfolio rebalancing lies at the very heart of ongoing global central banks interventions. By pushing down expected returns on low risk assets, central bankers are attempting to force investors up the risk curve (read: buy equities), hoping that the induced wealth effect boosts the economy. But as they accumulate vast amounts of bonds, they are also becoming the marginal buyer in that market. And a relatively price insensitive marginal buyer too, since their primary goal is not to generate an investment return but to support their countries financial system. In a context of low economic growth, this is likely to put a floor under government bond prices a cap on yields. We would thus view a move in the 10-year UST yield up toward 2.25% as an attractive entry point.

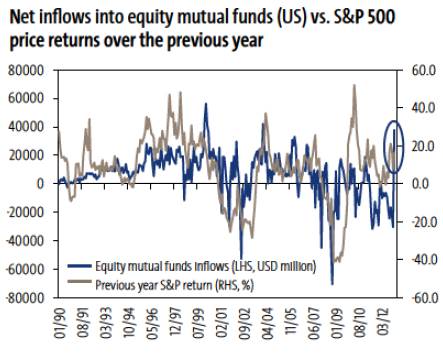

Looking at mutual fund flows, the pick-up in the first weeks of 2013 is typical following strong equity returns (middle chart), as there is a reactive aspect to flows into equities. Interestingly, these flows did not come at the expense of bond funds: while equity funds saw USD 38 bn of fresh inflows in January, after ten consecutive months of outflows, USD 33 bn continued to flow into bond funds on top of a USD 26 bn monthly average over the past 12 months.

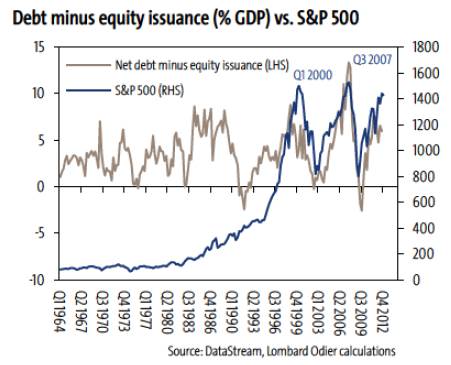

Finally, we would caution that the two latest episodes of large net debt issuance to finance stock buybacks corresponded to market extremes: 2000, 2007 (lower chart). This adds to other red signs, particularly on US equities, such as investor complacency, rich valuations and diminishing QE marginal effectiveness (or worse: talks of a QE exit strategy by some Fed members).

All told, far from envisaging a sustained and large equity rally on the back of a great rotation, our best case scenario would be for the equity rally to lose some steam, and the worst case scenario for it to experience a significant sell-off. Protect your portfolio, and be ready to move out of equities back into government bonds when yields normalize. A theme for 2013 might well actually be the rotation out of equities and back into bonds!

Source: www.lombardodier.com

|