|

After more than a decade of underperformance from traditional value factors, many value managers might be in the mood to sing the songs that remind them of the good times, the songs that remind them of the better times

Is the style dead, or just resting? We would argue its not quite dead.

First, a review of the facts:

- Value indices, like the Russell 1000 Value, have trailed growth indices like the Russell 1000 Growth, for seven of the past 11 years, underperforming significantly over that entire time period.

- Traditional value factors, like low price-to-earnings (P/E) and low price-to-book (P/B), have failed to add value after decades of showing their power.

Are Traditional Value Factors Still Relevant?

There are possible and even plausible explanations: value stocks have had slower earnings growth or have not been earning their cost of capital in some areas. Some have even proposed the idea that the traditional value factors no longer work.

This last group argues that value has done well, but that the traditional measurements are wrong. Essentially, this group argues that value has worked, but quality, momentum and industry biases have caused managers to miss the power of value. Ultimately, we believe this groupthat well refer to as the value has changed campis extrapolating from a decade where cheapness and/or mean reversion didnt work and forecasting that will continue. Im bolding these terms as they are potential behavioral errors!

How Have Value Factors Performed?

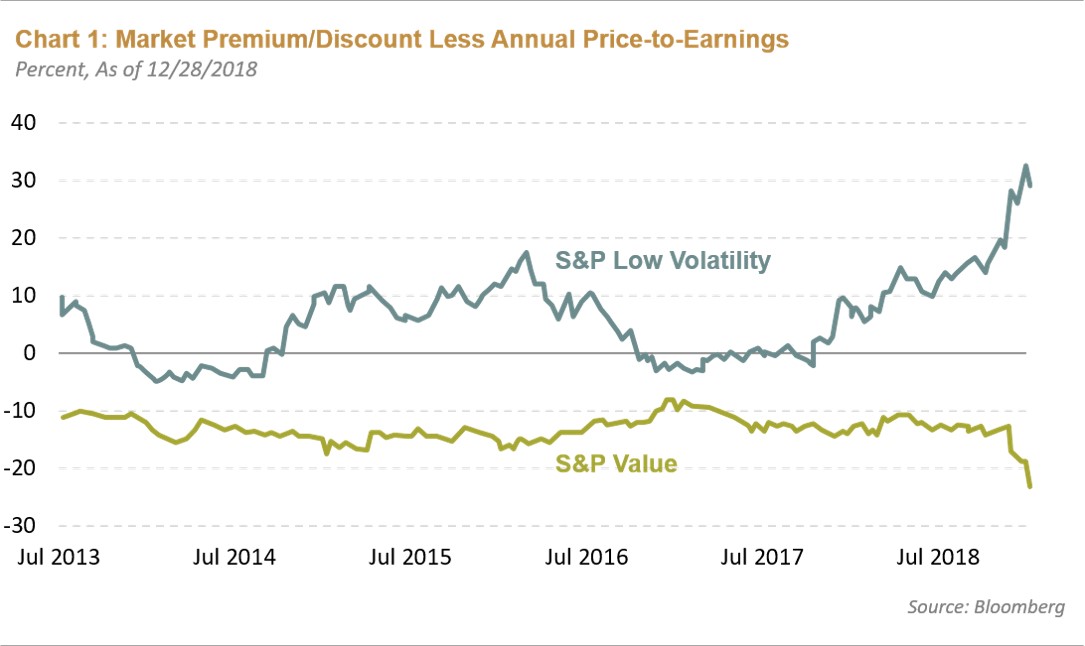

By one view, it would be an odd point in the economic and market cycle for value factors to start outperforming, given that we are a decade into the expansion. Value factors have historically outperformed at early stages of an economic expansion. Its been odd that value factors havent outperformed when the U.S. or global economy has come out of soft patches during the cycle. We can also layer on how low-volatility stocks have performed, which had the look of a parabolic bubble in late 2018:

To think that value might not work ever again would almost be suggesting that human nature has changed. If we think about why value investing works, its because people get too negative on a company/industry and the price declines to a level that discounts more problems than actually exist. Companies with good balance sheets trading below tangible book value or at single-digit P/E ratios might be a good place to look for these situations, as investors might be incorrectly estimating downside risks. A large number of value sectors have controversy around themthink autos, airlines, energyand history would suggest the market is overestimating the risks in at least some of these areas.

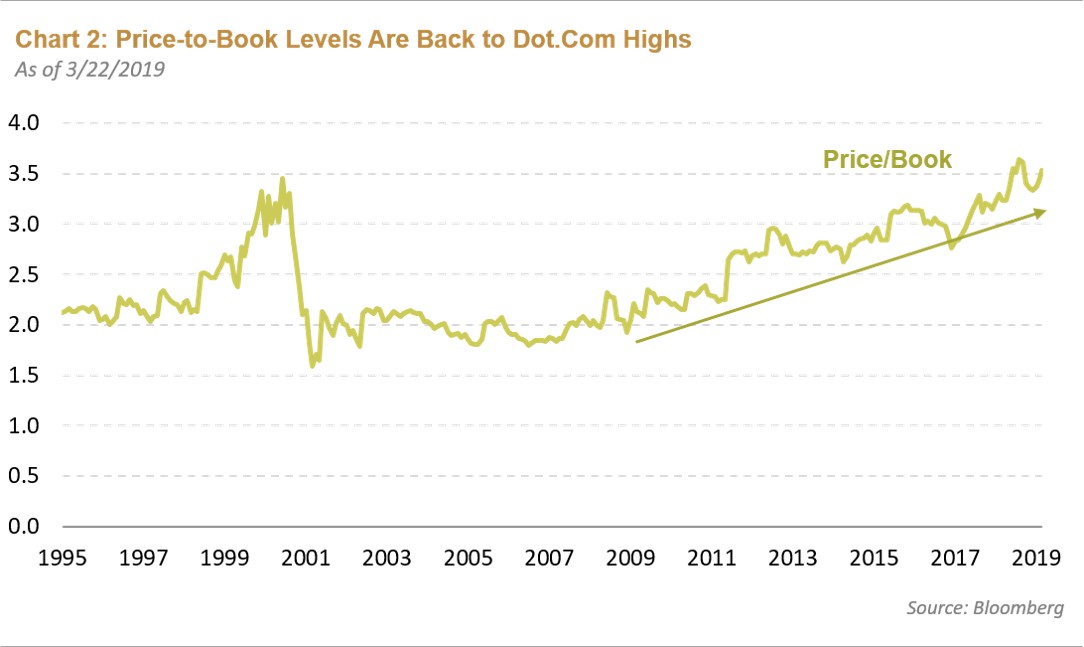

Some measures are back to tech bubble-like levels; for one, the P/B ratio of the Russell 1000 Growth is at a level unseen since 2000, while the Russell 1000 Values P/B ratio is relatively normal.

Where Are We in the Cycle?

On another view of the cycle, one could take the view that weve had three mini-recessions along the way: the 2011 Eurozone crisis, a 2015-16 profit recession, and the 2018-2019 global growth scare or slowdown that currently seems to be showing up in economic data. In this view, 2019 would absolutely be a year where value might do well, as value often does well coming out of recessions and/or slowdowns. Add in that it really wasnt until 2016 that the bottom 80% of households started seeing meaningful income growth, and this looks more like an environment where were in the third year of an expansion, rather than one past a decade in length. Some of this can also be seen in the below-average recovery growth in this longer cycle, which has also been a reason that this cycle had support for being abnormally long.

Is Value Investing Dead?

While we acknowledge the challenges facing value factors, we hardly think the style is dead. To summarize, these are the four main reasons to think that a value cycle might be on its way:

1. A period of underperformance this long is unprecedented.

2. Although it would be an odd time in the economic cycle for value to lead, this has not been a typical economic cycle and we may be in a growth scare right now that provides catalysts for value outperformance.

3. Valuation gaps between value and growth, and value and low volatility stocks, are wide.

4. Human behavior has not fundamentally changed.

|

Groupthink is bad, especially at investment management firms. Brandywine Global therefore takes special care to ensure our corporate culture and investment processes support the articulation of diverse viewpoints. This blog is no different. The opinions expressed by our bloggers may sometimes challenge active positioning within one or more of our strategies. Each blogger represents one market view amongst many expressed at Brandywine Global. Although individual opinions will differ, our investment process and macro outlook will remain driven by a team approach.

|

|