|

On the evening of Oct. 30, 1938, millions of Americans tuned their radios to CBS and heard Ramón Raquellos orchestra playing La Cumparsita. The popular tango music was interrupted by a news bulletin about explosions of incandescent gas on the planet Mars and a subsequent report of a huge, flaming object landing on a farm in New Jersey. If you had not heard the introduction to Orson Welles interpretation of The War of the Worlds, you would have been excused for thinking that the sky was falling. Thousands of frightened people called the police in a panic.

While entertainment has changed in the intervening decades, we are no less susceptible to panic. Today in financial markets the most overplayed story is that we are at risk of some manner of imminent crisis, whether its Europe facing deflation, Japans Abenomics experiment failing, China heading toward a real estate crisis or problems in any number of other countries from Ukraine to Thailand.

Heightening these worries is the fact that both equities and fixed income have rallied in tandem and fears of asset bubbles exist in categories from high-yield bonds to technology stocks. Especially with credit, some investors have begun to fear that a crisis must be around the corner. After all, with valuations evocative of 1993 or 2005/2006, logic suggests that what might come next could be akin to the massive bond-market correction of 1994, or the credit-market freeze of 2007 and the full-blown meltdown that followed in 2008.

But to connect the dots in that manner would be a mistake. Mays rally in fixed income was helped by strong capital flows. Liquidity from central banks globally and little expectation of any policy misstep means we are some distance away from any significant crisis. Now we are in the late stages of a bull market cycle, which while difficult to navigate can still be profitable for astute investors.

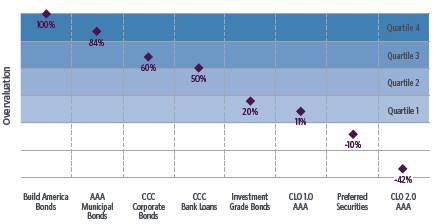

Degrees of Overvaluation

At Guggenheim we rank fixed-income assets in quartiles of overvaluation and current valuations make for an unattractive picture. Some high-yield credit is in the third quartile of overvaluation, for instance CCC-rated bonds and bank loans. Among municipal bonds, Build America Bonds are in the fourth quartile of overvaluation. There are still pockets of value Collateralized Loan Obligations, preferred stock and some investment-grade debt but the bottom line is that across the spectrum of fixed income, the level of overvaluation has increased dramatically over the last six to eight weeks.

U.S. Credit Shows Signs of Frothiness

Source: Credit Suisse, Barclays, Bank of America Merrill Lynch, Guggenheim Investments. Data as of May 30, 2014.

Markets that are overvalued and become more overvalued are called bull markets, and we are certainly in a bull market for credit. Despite tight spreads, history tells us that credit spreads can tighten further. When we started to reach the nosebleed levels of overvaluation in 2005 and 2006, Guggenheim bought higher-quality fixed-income assets so that when the downturn came, we did not have to suffer large credit losses. For the last five or six years, credit risk has been cheap, and it has worked really well for us. Now we have begun shifting gears, and the preservation of capital is the No. 1 objective, not taking on more risk.

Thats why we in recent weeks have bought agency mortgage pass-throughs from Fannie Mae and Freddie Mac something we have not done since before the 2008 financial crisis. With yields of 3.25 percent, a seven-year duration and U.S. government backing, it is an asset that now makes sense to us. Agency debt typically returns principal and interest annually amounting to 6-8 percent of face value, allowing us to reinvest at better yields when interest rates rise.

Crisis What Crisis?

When bull markets mature, investors fear a coming crisis. Today there are plenty of candidates from Europe to China to Thailand. But bull markets climb a wall of worry and there are reasons now not to expect a looming crisis.

1. Central Bank Liquidity

The No. 1 reason staving off crisis is that the world is afloat in a sea of liquidity. Every major central bank is pumping money into the economy. In early June, the European Central Bank employed a combination of innovative policies including negative interest rates and another long-term refinancing operation facility to combat low inflation and to encourage banks to lend rather than stockpile deposits. Europe is turning on its liquidity engine just as the U.S. Federal Reserve is tapering off its liquidity burst of the last few years.

2. U.S. Monetary Policy

Bull markets do not die of old age. Instead, they typically die of a policy mistake when central banks raise interest rates too quickly and snuff out an expansion or raise them too late and fail to slow economic overheating, often after certain asset prices have reached unsustainable levels. There is little reason now to expect such a policy mistake from the Fed, which is unlikely to start raising rates until late 2015 and possibly into 2016.

The concern is that for the first time since the Great Recession, inflation is starting to become an issue. We have passed the bottom in terms of good price behavior and leading indicators tell us to expect inflation to rise by another 50 basis points over the next 12 months. Having grown up in the 1970s, its hard for me to say inflation at 2.5 percent or 3 percent is a problem. But it could become an issue sometime in 2016 and if the Fed sees inflation north of 2 percent, that would be the basis for it to start raising interest rates.

For now, Fed Chairwoman Janet Yellen has made it clear that she takes the employment component of her mandate very seriously and that she wants to get America back to full employment. Fed policymakers have been troubled by the decline in the labor force participation rate during the current expansion, and the reasons for its fall have been the subject of vigorous debate among Federal Open Market Committee members. Some Federal Reserve policymakers fundamentally believe that the participation rate, which has fallen about 3 percentage points over the last few years, is due to rebound, despite a recent fall of 0.4 percent since March. The idea is that discouraged workers are going to see they can get a job again, and they are going to go back to work. If the labor participation rate does start to rise, that would cause the Fed to delay tightening. Some would even argue that the participation rate may not rise until the unemployment rate falls below that level associated with stable prices the non-accelerating inflation rate of unemployment, or NAIRU, and the Fed might experiment with lower levels of unemployment before raising interest rates.

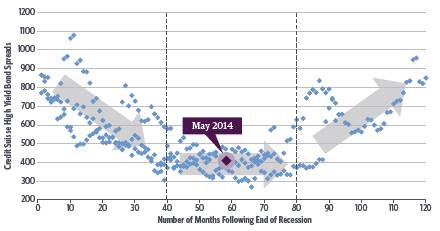

Credit cycles typically only end after corporate defaults start to spike, which normally happens 12-24 months after the Fed starts raising rates. That suggests this bull market could continue until 2017 or 2018, depending on when you expect the Fed will start raising rates.

Spreads Should Not Widen for Another Two Years

Source: Credit Suisse, Guggenheim Investments. Data as of April 30, 2014

A Flood of Capital

Underpinning the U.S. rally in bonds in May was a flood of capital into the United States. Foreign investors increased holdings of U.S. Treasuries by almost 4 percent to $5.95 trillion in the 12 months ended in March. That increased demand also has been evident in rising bid-to-cover ratios. Through the end of May, investors have bid 3.07 times the $918 billion of notes and bonds sold by the U.S. Treasury since the beginning of this year, well above the 2.87 times average for 2013. This wave of capital moving toward the United States has come at a time when we might have expected to see interest rates rising because the U.S. economy looks set to accelerate dramatically.

Instead, the 10-year U.S. Treasury note broke out of its tight trading range in May, closing at 2.44 percent on May 28 its lowest yield since June of last year. Notwithstanding the technical retrenchment that saw yields on 10-year U.S. Treasuries rise to 2.60 percent in early June, yields could now be headed to 2.2 percent or lower, just as the outlook for the U.S. economy is starting to brighten. Regardless, if rates were to continue declining from here it would signal that we are in for a period of sustained low interest rates.

Capital flows have come as a result of low yields in Europe, Japan and elsewhere. In Europe, the risk is that the euro will depreciate. That makes buying U.S. Treasury bonds and other U.S. assets attractive because the local currency could depreciate and interest rates are so significantly higher in the United States than in Europe. On June 6 in Germany, 10-year government bunds traded at 1.35 percent, compared with 10-year U.S. Treasuries at 2.58 percent, so, German investors seeking yield certainly want to look at the United States.

For Japanese investors it is a similar picture U.S. Treasuries at 2.58 percent look cheap compared with 10-year Japanese government bonds yielding 60 basis points. And legislation in Japan now allows larger allocations overseas by pension funds.

Investment Implications

With no pending crisis expected thanks to central bank liquidity and a bias among Fed policymakers to keep interest rates low, the recent bull market for credit spreads is alive and well, supported by surging capital inflows, which have also helped U.S. stocks hit fresh highs.

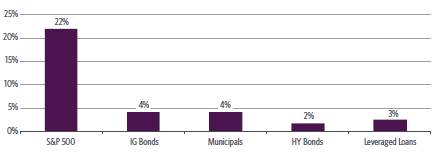

All Boats Rise Before Fed Tightening

Source: Credit Suisse, Barclays, Bloomberg, Guggenheim Investments. Data as of March 31, 2014. *Note: Average price performance in the 12 months prior to Fed tightening cycles in 1983, 1986, 1994, 1999, and 2004.

Bull markets have three phases. The first is the recovery, when prices are very depressed, the second is built on strong fundamentals, and the third is the speculative phase.

Clearly the Federal Reserve is increasingly risking the possibility of allowing the U.S. economy to overheat. Given its preoccupation with reducing unemployment while tolerating (if not even encouraging) an increase in inflation, the central bank is setting the stage to drive markets into what ultimately may prove to be unsustainable levels of overvaluation. Most likely over the course of the next 12 to 24 months we will move into this bull markets speculative phase.

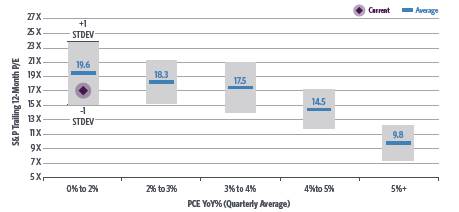

U.S. Equities Valuations High but Have Room to Run

Source: Bloomberg, Guggenheim Investments. Data as of 1Q2014.

Back in 1938, many of the listeners who had tuned their radios into The War of the Worlds had minutes earlier been listening to Americas most popular radio show on a different channel NBCs Chase and Sanborn Hour, the hit variety show starring ventriloquist Edgar Bergen and his dummy Charlie McCarthy. When Bergen and McCarthy finished their first sketch, many people channel surfed and tuned into CBS. If they had stayed tuned to NBC, they would have avoided participating in the panic suffered by many who had heard the Orson Welles production.

Similarly, investors today could be best served by ignoring nervous sentiment and staying tuned to what central banks are encouraging us to do. After all, often the best profits of a bull market come in the speculative phase, so investors should not change their investment frequency just yet.

www.guggenheimpartners.com

Link to the original report

|