|

Abstract

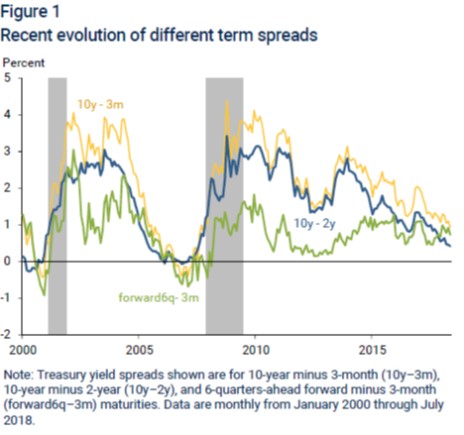

The ability of the Treasury yield curve to predict future recessions has recently received a great deal of public attention. An inversion of the yield curvewhen short-term interest rates are higher than long-term rateshas been a reliable predictor of recessions. The difference between ten-year and three-month Treasury rates is the most useful term spread for forecasting recessionswithout any adjustment for an estimate of the underlying term premium. However, such correlations in the data do not identify cause and effect, which complicates their interpretation.

Text Excerpt:

"Furthermore, when interpreting the yield curve evidence, one should keep in mind the adage correlation is not causation. Specifically, the predictive relationship of the term spread does not tell us much about the fundamental causes of recessions or even the direction of causation. On the one hand, yield curve inversions could cause future recessions because short-term rates are elevated and tight monetary policy is slowing down the economy. On the other hand, investors expectations of a future economic downturn could cause strong demand for safe, long-term Treasury bonds, pushing down long-term rates and thus causing an inversion of the yield curve. Historically, the causation may well have gone both ways. Great caution is therefore warranted in interpreting the predictive evidence."

Chart Excerpt:

Publication link

Reprinted from the Federal Reserve Bank of San Franciscos Economic Letter, 2018-20, August 27, 2018. The opinions expressed in this article do not necessarily reflect the views of the management of the Federal Reserve Bank of San Francisco or of the Board of Governors of the Federal Reserve System.

|