|

Back in December, 2011, I wrote about the insane leverage ratio at the Peoples Bank of China. The post generated a lot of buzz, but no one could actually answer the question of what happens when a central bank becomes insolvent.

We might get an answer to that question quicker than we expected. At current exchange rates, it will be one of the most expensive lessons in history.

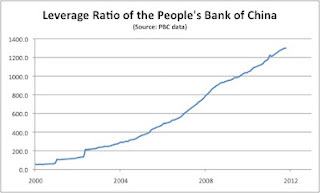

When I wrote the original post, the chart looked like this. The trajectory of the ratio meant it would pass 1400 in a few months.

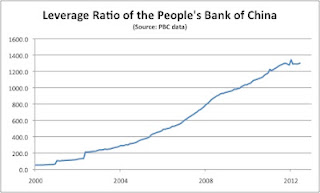

Today, it looks like this. Usually, when excessive leverage is involved, it is never a good thing (for the institution) when the amount of assets flat lines, or even slows down.

The Peoples Bank of Chinas balance sheet has definitely shown a noticeable slowdown. In the past, its balance sheet had the amazing ability to increase by a trillion renminbi every few months. The current balance seems to be stuck at around ¥28 trillion, which it passed in July, 2011. It broke through ¥29 trillion in January, but then fell back into the ¥28 trillion range. For our purposes, we can say that it will take over 11 months for the PBoC to add another trillion renminbi to its balance sheet. The last time it took the PBoC 11 months to add one trillion renminbi to its balance sheet was way back in 2002, so times have changed.

Remember, the PBoC had ¥28.6 trillion in assets at the end of June, 2012, but only ¥22 billion in capital. If its assets decrease by ¥22 billion (or -0.07%), it is insolvent. Since peaking out in January, 2012, the PBoCs balance sheet has lost ¥895 billion, so maybe it already is. Maybe nothing bad will happen. After all, who needs shareholders equity when you can print money?

Source: Mao Money, Mao Problems

|