|

Oxymorons ignore the Unhypothesized First Principle of Metaphysics by Aristotlethe principle of non-contradictionwhich guided the development of sciences for more than 2,500 years, until the emergence of quantum physics. In practice, oxymorons tend to develop at the margin and at the boundary conditions of a theory, or of a stable environment. Thus, they can reflect instabilities, contradictory forces, potential regime shifts etc. For this reason, they must be taken seriously.

World trade is, today, behaving like an oxymoron.

On July 20th, President Trump threathened to raise tariffs on all imports from China, which totalled $504 billion in 2017. The threat is more than eight times higher than the initial remedies announced by the Trump administration in March. The trade war has, indeed, escalated in the past six months.

World trade is one of the seven fundamental macro variables tracked by our macro AI model, TrackMacro, to measure equity risks. Following five months of cautiousness, TrackMacro turned deeply positive on world trade at the end of July and the end of August, exactly at the climax of the US-China trade war.

TrackMacros signal is thus counter-intuitive and requires interpretation.

An abnormal TrackMacro signal?

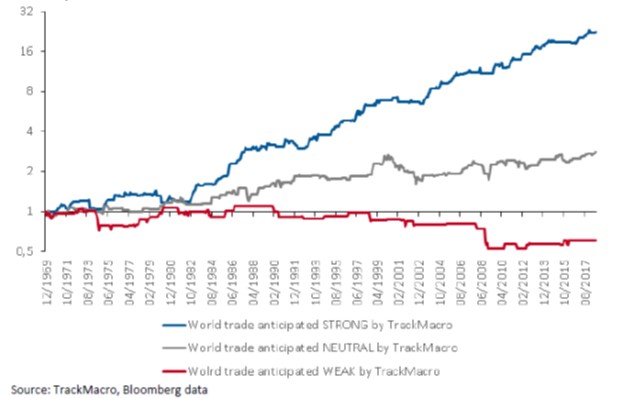

A first possible explanation could have been the deterioration of TrackMacros model of world trade risk. The following chart shows TrackMacros ability to successfully cluster word trade regimes and the consequences on equity returns. The model has not shown signs of weakness: neither during the last decade, as compared to long-term history, nor since it went live, three years ago.

Chart 1. MSCI World return when world trade is anticipated strong, neutral, or weak by TrackMacro

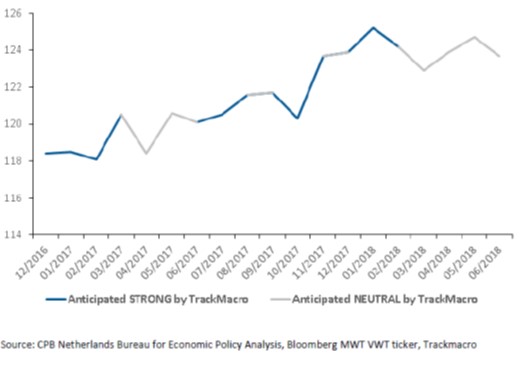

Looking at the most recent short time-scale, i.e. the 2017 market rally and the 2018 regime shift, the following chart shows TrackMacros anticipation of world trade in volume three months ahead of official publications.

TrackMacro has been able to navigate successfully high frequency regime shifts in the recent past. The conclusion is that we have no evidence of any deterioration of TrackMacros model, on any time-scale.

Chart 2. World trade in volume and TrackMacros anticipation in 2017 and 2018

An abnormal elasticity?

A possible explanation for higher trade levels during a trade war could be the stocking-up effect, anticipating higher tariffs at a later date. The abnormal elasticity of trade volume to trade risk would not, then, be reflecting a better situation than expected for today, but a worse one anticipated for tomorrow.

The same abnormality was observed in France at the beginning of the XXth century. Any increase in the price of bread lead to an increase in the demand for bread. The explanation was that poor people spent a significant portion of their purchasing power to feed their family. They consumed mostly bread and vegetables, and only sometimes, meat. When the price of bread increased, they could no longer afford to buy meat, and in turn, chose to consume more bread. Positive elasticity at the time reflected a deterioration of economic conditions, not an improvement.

Conclusion

Why is trade the focus of this note?

Simply because international business is key in a systemic phase transition. Whats new today is that local macro variables such as inflation, growth, and relative competitiveness are diverging among major economic centers.

The 2017 alignment of planets is over. The US is booming, both economically and financially; Europe is at the tipping point; China is slowing down and devaluating. Emerging markets, at the periphery of the centers competition, are being severely hit with the global political and trade war, and by a shortage of USD.

As long as world trade benefits from global adjustments, whatever the reasons, TrackMacros asset allocation favors risk assets, with the exception of specifically weak areas. For example, the model successfully spotted, for a while, local country weaknesses with Italy and Turkey.

Entering September, TrackMacro continues to select risk asset investments in America, but reduces exposure in the Eurozone, and cherry picks in Asia.

The oxymoron of world trade is at the drivers seat.

|