|

A very interesting paper on a topic that is often misunderstood. In addition to the abstract and the conclusion, we have selected three charts; however, we recommend you to read the full text.

Abstract

The public often gauges the strength of the U.S. economy by the performance of the manufacturing sector, especially by changes in manufacturing employment. When such employment declines, as has been the trend for many years, it is often assumed to be evidence of the slow death of U.S. manufacturing and an associated rise in imports. This article outlines key trends in U.S. manufacturing, especially the strong performance of manufacturing output and productivity, and their connection to both exports and imports. The authors use ordinary regression, causality, and cointegration analyses to provide empirical evidence for the positive role of imports in boosting manufacturing output. Policies to bolster exports at the expense of imports would significantly harm U.S. manufacturing. (JEL O4, F4, E3)

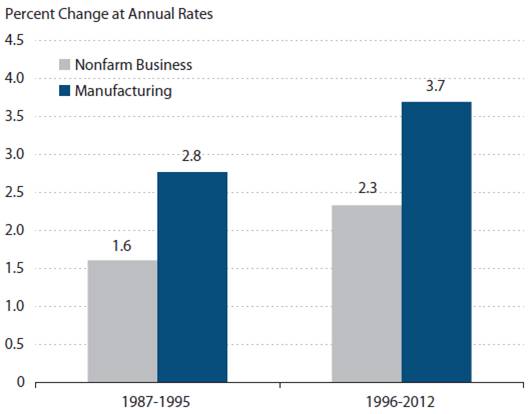

Labor Productivity Growth (1987-1995, 1996-2012)

Source: Bureau of Labor Statistics.

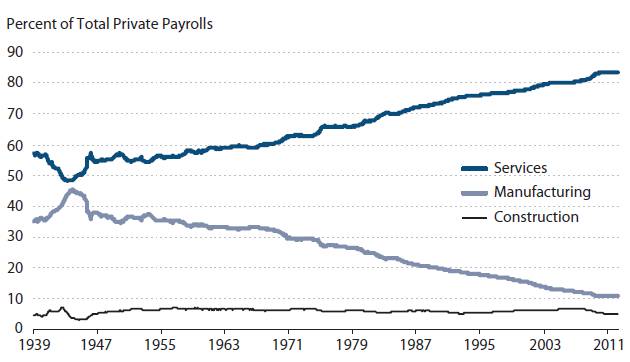

Private Employment Shares in the Service-Producing and Manufacturing Sectors

Source: Bureau of Labor Statistics.

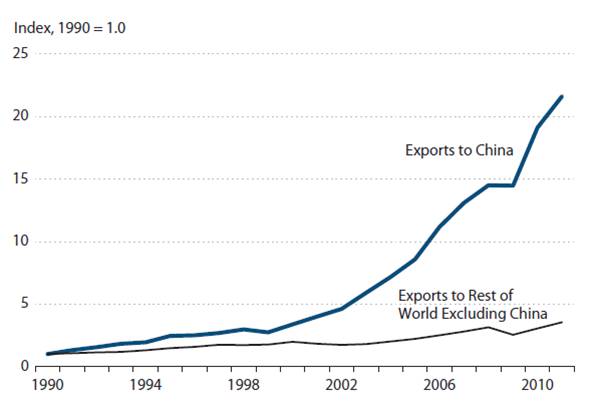

U.S. Export of Goods

Source: Department of Commerce (Bureau of the Census) and Council of Economic Advisers.

Conclusion

"U.S. manufacturing suffered a massive decline during the recession in 2008-09, but it has made an impressive comeback. Unfortunately, the same cannot be said for manufacturing employment. Behind the recent trends is relatively rapid manufacturing productivity growth; this growth could have led to dramatic gains in output with unchanged employment, but manufacturing demand is not as responsive to gains in income. The income gains from manufacturing productivity growth boost demand for manufacturing output relatively less than the demand for services. Thus, most of the gains appear in services output and employment with a relatively smaller rise in manufacturing output. As a result, manufacturing employment is displaced to produce services that are relatively more in demand as a result of manufacturing-led economic growth. The same phenomenon has characterized agricultural development for over a century.

In the 1980s, these developments were referred to as the deindustrialization of America and the hollowing out of the U.S. manufacturing industry. Much of the blame was laid on outsourcing and offshoring to foreign subsidiaries and foreign firms. In fact, Tatom (1988) explains that the 1980s were characterized by a boom in manufacturing output and productivity that led economic growth in general and led demand for manufactured goods to outpace capacity growth in manufacturing. As a result, imports boomed along with domestic manufacturing output. The same has been true in the past decade. In recent years, the weakness of manufacturing employment, especially during the recession, has rekindled passions about the death of manufacturing. Continuing globalization has led critics to once again seize on international forces as both the culprit (imports) and the potential solution (increased exports) to the manufacturing problem.

Several other trends in manufacturing continue to be important factors in understanding recent developments. Manufacturing is dominated by some very large firms: Fewer than 10 percent of firms control almost 90 percent of manufacturing assets. Nonetheless, about 45 percent of the estimated 137,770 manufacturing firms have less than $10 million in assets. Output remains very volatile, especially in the durable goods sector where demand is readily postponed during recessions and resumed in expansions. This is less the case in nondurable manufacturing and usually barely noticeable in service industries.

The unusually strong performance of manufacturing productivity has largely been the result of rising total factor productivity and relatively rapid growth in the capital-to-labor ratio in manufacturing. Both have accelerated since 1995 and increased even further in the latest recession, recovery, and expansion. Evidence here also shows the expected positive link between strong productivity growth, the relatively high real rates of return across the manufacturing

sector, and the deepening of capital per worker or per labor hour.

Our analysis focuses on the role of exports and imports in affecting manufacturing performance. Surprisingly, we find that imports have played a critical positive role in boosting manufacturing output in the United Statesmuch more so, in fact, than exports. We find no discernible influence of export growth on manufacturing growth, but there is a strong positive influence of import growth on manufacturing growth. Many industry, labor, and political leaders believe that boosting manufacturing growth will require limiting imports through favorable preferences for domestic purchasing and raw material and capital goods sourcing, perhaps through quotas, tariffs, domestic content legislation, or simply discriminatory preferences. However, reliance on imports has been a strong positive influence on manufacturing output and productivity. Moreover, there is no discernible gain to manufacturing growth that could arise from new policies proposed to boost exports.

We present causality tests indicating that neither imports nor exports cause manufacturing growth. Instead, both exports and imports are led systematically by prior growth in manufacturing. Thus in the recent recession, a large subsequent decline in imports and exports should not have been a surprise. The importance of imports to domestic manufacturing performance cannot be overstated. Goods imports equal more than 100 percent of manufacturing value added, so they account for more than half of the gross output and sales of domestically produced products.

Intermediate goods imports and capital goods imports are the lifeblood of U.S. output. Exports account for a much smaller share of manufacturing value added. While development of foreign markets offers an opportunity for outsized growth, the success of manufacturing has not been as critically dependent on new markets for sales as for new markets for materials and capital goods."

|