|

Golds purchasing power has remained remarkably stable in the past 400 years, at least until the end of the Bretton Woods system in August 1971.

The ensuing debasement of major currencies created a new competition between gold and currencies to attract world savings, and also between currencies themselves.

Crucially, gold refused to falter in the face of competition. Quite to the contrary, the metal remained, 50% of the time, the best money to secure savings from 1972s onwards.

Why?

Because, as J.P. Morgan stated in his testimony before Congress in 1912, Gold is money. Everything else is credit.

This letter looks to describe the terms of the competition and identify the best moments to buy currencies rather than gold.

Gold: an effective store of value

Professor Roy Jastram of the University of California completed, in 1976, a long-term analysis of golds purchasing power. The research was updated by Jill Leyland in 2009.

Jastram concluded that gold, as well as silver, had protected investors purchasing power across centuries. Figure 1 on the next page illustrates the stability of gold from the mid-16th century to the end of the gold standard, and its subsequent volatility.

Fig 1. Purchasing power of gold since 1560

Source: World Gold Council. Prices indexed at 100 in 1930

The competition across currencies in the last 50 years

Major economic zones compete to attract excess savings. Since 1972, they have faced a dilemma: they cannot simultaneously remunerate cash and equity risk effectively. An expensive cash favors the rentier at the expense of the entrepreneur, and vice versa.

The consequence is the emergence of a two-fold competition across major economic and monetary zones, on the cash side and on the equity risk side.

TrackMacro 2.0, launched this summer, approaches this competition in a simple manner. Cash remuneration includes interest rates and foreign exchange gains and losses. Its attractiveness depends on monetary policies as well as on cultural and political factors. Some countries, such as Germany before the Euro or China in the last ten to fifteen years, tend to favor the rentier. Others, such as the USA, tend to favor the entrepreneur.

The ranking across zones evolves, but at longer timescales than emotional trading in market finance. It follows from this that an international investor can benefit from the competition by investing their cash and their equity risk premia in a differentiated manner, always selecting the best zone both on cash and risk.

TrackMacros way to identify the best zone is to measure the (rolling) past year remuneration, betting on the inertia of the ranking.

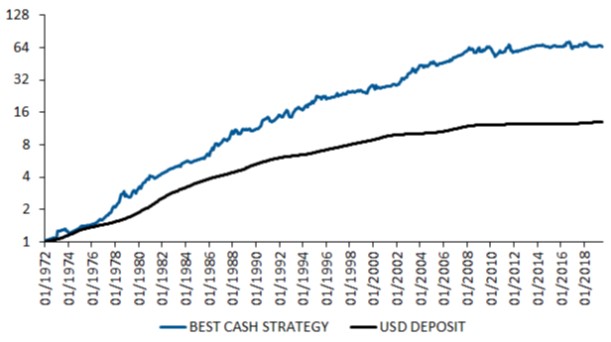

Below, Figure 2 compares the return of a Best Cash strategy, tracking the remuneration of five major currencies (USD, EUR, GBP, JPY, CNY), against USD deposit.

Fig 2. USD deposit returns vs. Best Cash Strategy

Source: TrackRisk by Gavekal Intelligence Software

The Best Cash strategy returned 8.5% per annum, as compared to 5.6% for USD cash deposits. Furthermore, the alpha generation is remarkably stable for the past circa 50 years. The strategy is robust.

But, what about gold?

The competition between gold and major currencies

Gold is money and competes with major currencies because of its longstanding track record as a store of value.

When currencies pay well, gold, which does not provide interest, is useless. However, when major central banks opt for low cash remuneration, targeting the euthanasia of the rentier, gold re-emerges as an investment alternative.

Gold, however, is much less liquid than major currencies, hence its propensity to spike when central banks do not pay enough cash placements.

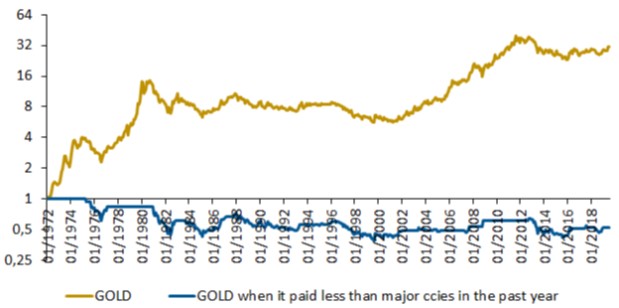

We use the same method as the one proposed by TrackMacro to measure the ranking between gold and an average basket of the five major currencies mentioned above. If gold pays more than the basket in the (rolling) past year, then it is time to get rid of currencies and switch to gold!

50% of the time, currencies pay enough to satisfy the rentier and gold is useless, as shown in Figure 3 below.

Fig 3. Gold return when currencies pay enough

Source: TrackRisk by Gavekal Intelligence Software

Figure 3 shows that, since the end of the gold standard, gold itself has lost its status as a store of value 50% of the time. Gold investors lose 2.3% per annum and 6.2% per annum in real terms.

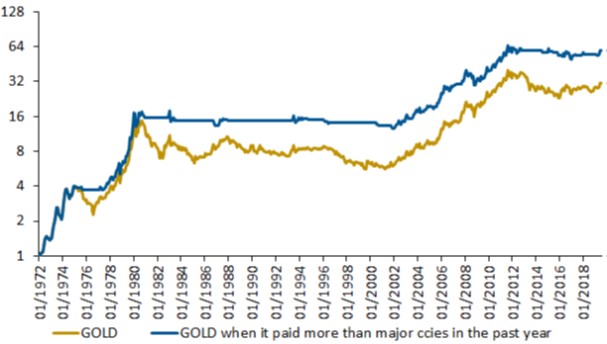

The story is, however, very different the other 50% of the time, when central banks cut cash remuneration, which is equivalent to raising tax on depositors. Gold then thrives and provides +19.1% capital gain per annum on average, as shown in Figure 4 on the next page.

Fig 4. Gold return when currencies pay not enough

Source: TrackRisk by Gavekal Intelligence Software

Investing in gold when it is only worth it provides much higher returns than holding gold permanently, and much lower drawdown risk.

Conclusion

Gold is still there, hiding in the marketplace, and waiting for currency debasement from major monetary centers.

On January 31st this year, gold took the lead against our currency basket, at a price of 1321. It gained +15% since then, and continues to lead the race.

|