|

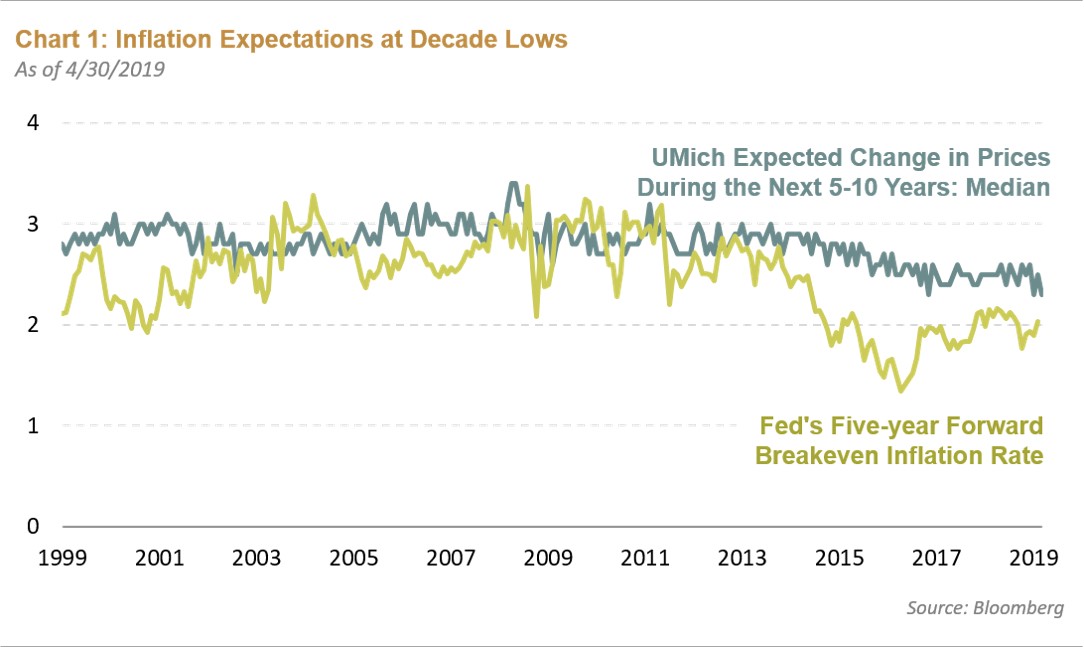

The 5-year forward inflation breakeven derived from Treasury and the Treasury Inflation-Protected Security (TIPS) market prices is around 2%. The University of Michigan Survey of expected inflation shows a similar trajectory (see Chart 1). This matters because it limits how high nominal short rates can rise before the next recession. In turn, this proximity to the zero lower bound constrains monetary policy options in the eventual next recession. And while the next recession may or may not be a long way off, the best time to fix the roof of your house is when its sunny outside.

So why are inflation expectations so low in the first place? Well, the Fed states that inflation at a rate of 2% is most consistent over the longer run with its dual mandate of maximum employment and stable prices. However, in its effort to be forward looking, the Fed tends to start hiking well before inflation reaches that level. As a result, inflation rarely spends much time above 2% (see Chart 2). If the Fed was properly delivering on its inflation target, inflation would spend about half the time above and half the time below the target. In other words, there should be a certain symmetry to the inflation target.

Former Fed Chair Janet Yellen alluded to this when she argued a few years back about letting the economy run hot. Her arguments did not gain traction at the time, but they have resurfaced. Indeed, it is likely that a fundamental shift is underway in terms of how the Fed conducts monetary policy. In the words of John C. Williams, President of the Federal Reserve Bank of New York, something like an average inflation targeting would help achieve the target over time. During downturns when policy is constrained inflation will be a little low. During times of economic expansion and booms, like today, inflation would be expected to be above 2%. Back in November, the Fed announced plans to review its monetary policy framework. In June, the Federal Reserve Bank of Chicago will host a research conference which will provide the academic support for any changes in the framework. Skeptics may scoff at the fact that a central bank that cannot consistently hit its 2% target is about to set a more ambitious target. But if monetary policy is largely a game of expectations, shifting to a more dovish framework just as the unemployment rate hits 50-year lows would go a long way.

If the worlds central bank changes its monetary policy framework this year, the market impact could be huge. Its hard to discern investment implications without knowing details yet, but this could alter the way we think about Treasuries versus TIPS, fair value spreads for emerging market bonds, the dollar, and gold.

|

Groupthink is bad, especially at investment management firms. Brandywine Global therefore takes special care to ensure our corporate culture and investment processes support the articulation of diverse viewpoints. This blog is no different. The opinions expressed by our bloggers may sometimes challenge active positioning within one or more of our strategies. Each blogger represents one market view amongst many expressed at Brandywine Global. Although individual opinions will differ, our investment process and macro outlook will remain driven by a team approach.

|

|